Get a free, no-obligation financial consultation. Schedule Now

Please note by using any of the links provided for your convenience you will be leaving Fidelis Wealth Advisors website. The hyperlinks are to websites and servers maintained by third parties. We do not control, evaluate, endorse or guarantee content found in those sites. Your use of such sites is at your own risk.

Please note by using any of the links provided for your convenience you will be leaving Fidelis Wealth Advisors website. The hyperlinks are to websites and servers maintained by third parties. We do not control, evaluate, endorse or guarantee content found in those sites. Your use of such sites is at your own risk.

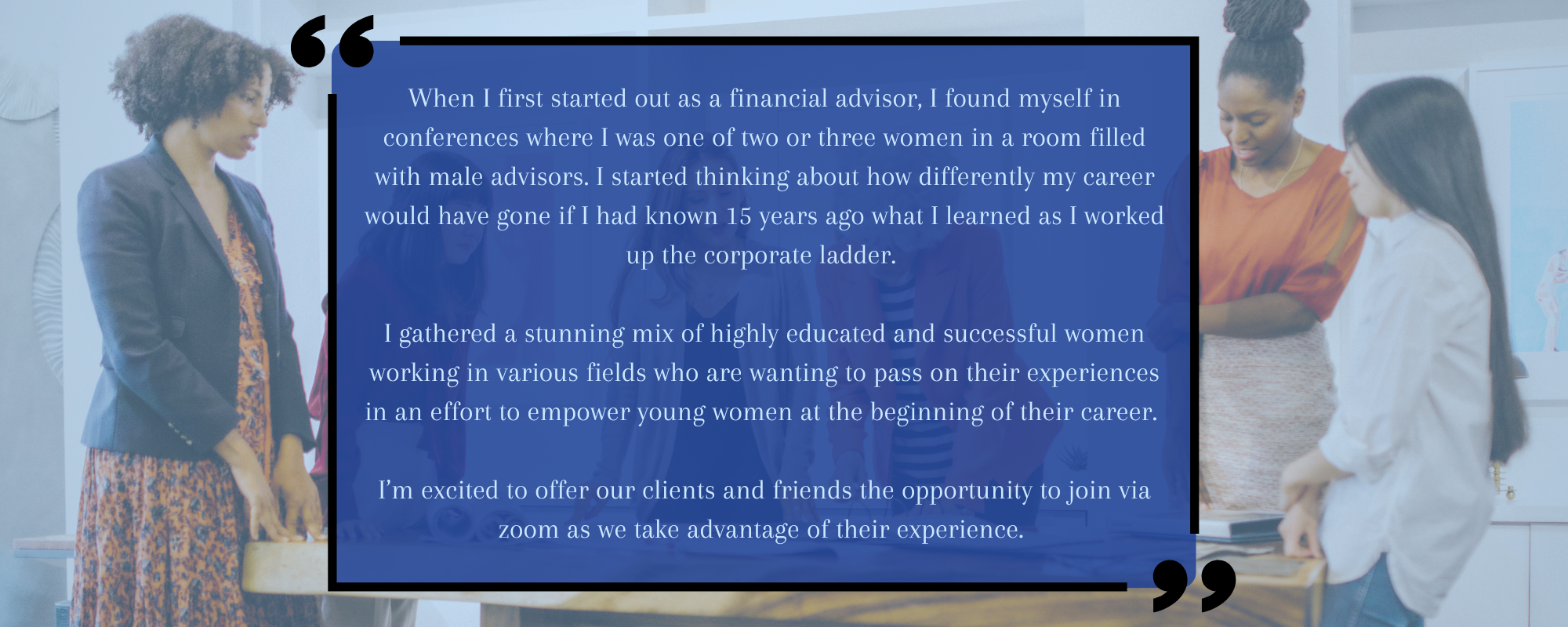

Author: Lorie

Welcoming Women to the Room – Codie Winslow

Posted on

Welcoming Women to the Room – Codie Winslow

Created by: Lorie Jones

Check out Codie Winslow’s presentation on how she transformed the Douglas County Clerk’s office into a productive workplace by emphasizing staff strengths and creating a dynamic environment.

Don’t miss out on Codie’s tips for attracting potential employees to your workplace by fostering a strong company culture towards the end of the video.

We extend our gratitude to Codie Winslow for sharing her experiences and techniques to “Welcome Women to the Room.”

Don't miss out on our next speaker Amy Sherman! Register today:

Find useful tools to improve your professional development? Continue watching our Welcoming Women to the Room series:

Please note by using any of the links provided for your convenience, you will be leaving Fidelis Wealth Advisors website. The hyperlinks are to websites and servers maintained by third parties. We do not control, evaluate, endorse, or guarantee content found in those sites. Your use of such sites is at your own risk.

This blog is general communication being provided for informational purposes only. This information is in no way a solicitation or offer to sell securities or investment advisory services. It is educational in nature and not to be taken as advice or a recommendation for any specific investment product or investment strategy. This does not contain sufficient information to support an investment decision. Any investment or investment strategy mentioned may not be suitable for all investors or in their best interest. Statistical information, quotes, charts, references to articles or any other quoted statement or statements regarding market or other financial information is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. All rights are reserved. No part of this blog including text, graphics, et al, may be reproduced or copied in any format, electronic, print, et al, without written consent from Fidelis Wealth Advisors, LLC. Fidelis Wealth Advisors does not provide legal or tax advice. Please be advised to consult with your investment advisor, attorney or tax professional before making any investment decisions.

Check out Codie Winslow’s presentation on how she transformed the Douglas County Clerk’s office into a productive workplace by emphasizing staff strengths and creating a dynamic environment.

Don’t miss out on Codie’s tips for attracting potential employees to your workplace by fostering a strong company culture towards the end of the video.

We extend our gratitude to Codie Winslow for sharing her experiences and techniques to “Welcome Women to the Room.”

Don't miss out on our next speaker Amy Sherman! Register today:

Find useful tools to improve your professional development? Continue watching our Welcoming Women to the Room series:

Please note by using any of the links provided for your convenience, you will be leaving Fidelis Wealth Advisors website. The hyperlinks are to websites and servers maintained by third parties. We do not control, evaluate, endorse, or guarantee content found in those sites. Your use of such sites is at your own risk.

This blog is general communication being provided for informational purposes only. This information is in no way a solicitation or offer to sell securities or investment advisory services. It is educational in nature and not to be taken as advice or a recommendation for any specific investment product or investment strategy. This does not contain sufficient information to support an investment decision. Any investment or investment strategy mentioned may not be suitable for all investors or in their best interest. Statistical information, quotes, charts, references to articles or any other quoted statement or statements regarding market or other financial information is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. All rights are reserved. No part of this blog including text, graphics, et al, may be reproduced or copied in any format, electronic, print, et al, without written consent from Fidelis Wealth Advisors, LLC. Fidelis Wealth Advisors does not provide legal or tax advice. Please be advised to consult with your investment advisor, attorney or tax professional before making any investment decisions.

Welcoming Women to the Room – Lisa Brown

Posted on

Welcoming Women to the Room – Lisa Brown, CFP®, CIMA®, GFP (USA)

Created by: Lorie Jones

Please watch as Lisa Brown discusses her personal experience juggling career and family life, while her husband “retired” to be a full-time Dad and the importance of money conversations along the way.

Don’t miss Lisa’s tips for finding windows of interaction with loved ones at the end of the video.

We are so grateful to Lisa Brown for sharing her experience and how she helps “Welcome Women to the Room.”

Don't miss out on our next speaker CODIE WINSLOW! Register today:

Find useful tools to improve your professional development? Continue watching our Welcoming Women to the Room series:

Please note by using any of the links provided for your convenience, you will be leaving Fidelis Wealth Advisors website. The hyperlinks are to websites and servers maintained by third parties. We do not control, evaluate, endorse, or guarantee content found in those sites. Your use of such sites is at your own risk.

This blog is general communication being provided for informational purposes only. This information is in no way a solicitation or offer to sell securities or investment advisory services. It is educational in nature and not to be taken as advice or a recommendation for any specific investment product or investment strategy. This does not contain sufficient information to support an investment decision. Any investment or investment strategy mentioned may not be suitable for all investors or in their best interest. Statistical information, quotes, charts, references to articles or any other quoted statement or statements regarding market or other financial information is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. All rights are reserved. No part of this blog including text, graphics, et al, may be reproduced or copied in any format, electronic, print, et al, without written consent from Fidelis Wealth Advisors, LLC. Fidelis Wealth Advisors does not provide legal or tax advice. Please be advised to consult with your investment advisor, attorney or tax professional before making any investment decisions.

Welcoming Women to the Room – Rachelle Morris

Posted on

Welcoming Women to the Room – Rachelle Morris, Managing Director

Created by: Lorie Jones

Please watch as Rachelle Morris discusses her experiences working in the high-pressure world of venture capital while also prioritizing her volunteer work with women and girls through organizations such as The Policy Project. Don’t miss Rachelle’s tips she wished she knew throughout her work experience including how to handle the uncertainties in life at the end of the video.

We are so grateful to Rachelle Morris for sharing her experience and how she helps “Welcome Women to the Room.

Find useful tools to improve your professional development? Continue watching our Welcoming Women to the Room series:

Please note by using any of the links provided for your convenience, you will be leaving Fidelis Wealth Advisors website. The hyperlinks are to websites and servers maintained by third parties. We do not control, evaluate, endorse, or guarantee content found in those sites. Your use of such sites is at your own risk.

This blog is general communication being provided for informational purposes only. This information is in no way a solicitation or offer to sell securities or investment advisory services. It is educational in nature and not to be taken as advice or a recommendation for any specific investment product or investment strategy. This does not contain sufficient information to support an investment decision. Any investment or investment strategy mentioned may not be suitable for all investors or in their best interest. Statistical information, quotes, charts, references to articles or any other quoted statement or statements regarding market or other financial information is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. All rights are reserved. No part of this blog including text, graphics, et al, may be reproduced or copied in any format, electronic, print, et al, without written consent from Fidelis Wealth Advisors, LLC. Fidelis Wealth Advisors does not provide legal or tax advice. Please be advised to consult with your investment advisor, attorney or tax professional before making any investment decisions.

Welcoming Women to the Room – Jessica Taylor, CPO

Posted on

We are so grateful to Jessica for sharing her experience and how she helps “Welcome Women to the Room.”

Find useful tools to improve your professional development? Continue watching our Welcoming Women to the Room series:

Please note by using any of the links provided for your convenience, you will be leaving Fidelis Wealth Advisors website. The hyperlinks are to websites and servers maintained by third parties. We do not control, evaluate, endorse, or guarantee content found in those sites. Your use of such sites is at your own risk.

This blog is general communication being provided for informational purposes only. This information is in no way a solicitation or offer to sell securities or investment advisory services. It is educational in nature and not to be taken as advice or a recommendation for any specific investment product or investment strategy. This does not contain sufficient information to support an investment decision. Any investment or investment strategy mentioned may not be suitable for all investors or in their best interest. Statistical information, quotes, charts, references to articles or any other quoted statement or statements regarding market or other financial information is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. All rights are reserved. No part of this blog including text, graphics, et al, may be reproduced or copied in any format, electronic, print, et al, without written consent from Fidelis Wealth Advisors, LLC. Fidelis Wealth Advisors does not provide legal or tax advice. Please be advised to consult with your investment advisor, attorney or tax professional before making any investment decisions.

Welcoming Women to the Room – Jessica Taylor, CPO

Created by: Lorie Jones

Please watch as Jessica Taylor discusses how to know and demonstrate your worth in your profession and your life. I haven’t found a better example of someone who is more aware of her value than Jessica. Make sure and watch through to the end where Jessica shares her tips on how to ask for and get a raise.

We are so grateful to Jessica for sharing her experience and how she helps “Welcome Women to the Room.”

Find useful tools to improve your professional development? Continue watching our Welcoming Women to the Room series:

Please note by using any of the links provided for your convenience, you will be leaving Fidelis Wealth Advisors website. The hyperlinks are to websites and servers maintained by third parties. We do not control, evaluate, endorse, or guarantee content found in those sites. Your use of such sites is at your own risk.

This blog is general communication being provided for informational purposes only. This information is in no way a solicitation or offer to sell securities or investment advisory services. It is educational in nature and not to be taken as advice or a recommendation for any specific investment product or investment strategy. This does not contain sufficient information to support an investment decision. Any investment or investment strategy mentioned may not be suitable for all investors or in their best interest. Statistical information, quotes, charts, references to articles or any other quoted statement or statements regarding market or other financial information is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. All rights are reserved. No part of this blog including text, graphics, et al, may be reproduced or copied in any format, electronic, print, et al, without written consent from Fidelis Wealth Advisors, LLC. Fidelis Wealth Advisors does not provide legal or tax advice. Please be advised to consult with your investment advisor, attorney or tax professional before making any investment decisions.

“Only when the tide goes out do you discover who’s been swimming naked.” Warren Buffett

Posted on

By: Sam Tenney, CFP, AIF

We are actively monitoring the news regarding Silicon Valley Bank (SVB) and other current economic events.

Why does this matter to you?

Rising interest rates and new banking regulations impact all investments. Could recent events with SVB, Signature Bank and others cause the Federal Reserve to pause raising interest rates? These are topics that will influence our investment positioning as we gather more clear information.

The closure of SVB is a big financial domino that has fallen, partially, as a result of the recent rapid increase in the Federal Reserve’s interest rate policy. SVB will not be the last domino to fall. This letter provides some insight into the recent events we are monitoring.

What happened?

Silicon Valley Bank (SVB) was the 16th largest bank in the US. SVB was the financing and banking partner of approximately half of all tech startup companies in Silicon Valley. SVB underwent a run on the bank (which means withdrawal requests exceeded cash on hand), late last week. The bank was shut down by the FDIC on Friday.

SVB was more unique than most banks, in that 97% of deposits held with the bank were over the $250,000 amount that the Federal Deposit Insurance Corporation (FDIC) insures. Thus, most deposits were uninsured and at risk of at least a partial loss. On Sunday, the FDIC in connection with the US Treasury department and Federal Reserve created a backstop for all deposits at this bank and others that have been shut down.

Why did it happen?

SVB tripled in size from 2019 to 2022 increasing from approximately $60 billion in assets to around $200 billion. As a result, the bank invested large amounts of cash in government bonds and mortgage-backed bonds at historical low interest rates. Then, the Fed Reserve raised rates at a historically fast pace last year, which led to the banks bond investments falling in value. In addition, SVB’s business niche of venture capital was slowing rapidly in 2022 into 2023. The bank sought to firm up their financial balance sheet, so they sold some investments, and then tried to raise more capital from investors. The timing of both, and the previously disclosed losses on their investment portfolio spooked investors and depositors, which sparked a rapid run on the bank. The FDIC took over the bank on Friday. Just three days earlier, Moody’s rating agency had listed SVB with an A credit rating.

Bottom line, SVB grew too fast without proper planning or risk management by their executives. Poor timing exposed SVB lack of preparation, thus when the Federal Reserve’s policy turned to aggressively raising interest rates, combined with a business slowdown, SVB’s management mishandled these hurdles and accelerated their own financial crisis. As the tide of low interest rates went out, SVB got caught without their clothing, as Warren Buffett famously stated in a previous financial collapse.

What did the government do?

Government (FDIC, Federal Reserve & US Treasury) decided on Sunday to back all depositors, not stock, or bond holders of SVB.

Why did the government do what they did?

The government is trying to prevent a run on other banks and to prevent a full scale financial crisis. To do this, they provided an implied guarantee (backstop) to SVB depositors. What this means is that all deposits (even those held above the $250k FDIC limit) will be protected. The government also wanted the customers of the bank to have access to their deposits, to minimize the disruption SVB closure had on its many business customers. Businesses relying on SVB would have experienced severe operational disruptions, and potential insolvency (which would have led to a large increase in unemployment), to prevent this, the government stepped in.

Doing so, it appears that the Federal Government has taken the risk out of having deposits over $250k at a bank (we are still trying to determine if this will become an explicit guarantee from the FDIC). It seems likely at this time that this change will apply to Signature Bank and any others going forward.

What does this mean for you?

It means more investment volatility as uncertainty continues. It means that we all have to better understand what rules we are playing by as investors, savers, and depositors.

I believe in human innovation, human ingenuity, and a growth mindset, as such, I believe we must continue investing for the long-term even with the all the noisiness of politics, greed, and headlines dominating the news each day.

Please call us if you have any questions.

This blog is general communication being provided for informational purposes only. This information is in no way a solicitation or offer to sell securities or investment advisory services. It is educational in nature and not to be taken as advice or a recommendation for any specific investment product or investment strategy. This does not contain sufficient information to support an investment decision. Any investment or investment strategy mentioned may not be suitable for all investors or in their best interest. Statistical information, quotes, charts, references to articles or any other quoted statement or statements regarding market or other financial information is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. All rights are reserved. No part of this blog including text, graphics, et al, may be reproduced or copied in any format, electronic, print, et al, without written consent from Fidelis Wealth Advisors, LLC. Fidelis Wealth Advisors does not provide legal or tax advice. Please be advised to consult with your investment advisor, attorney or tax professional before making any investment decisions.

Welcoming Women to the Room – Laycee Kolkman PE, PTOE

Posted on

Welcoming Women to the Room – Laycee Kolkman, PE, PTOE

Created by: Lorie Jones

Please watch as Laycee Kolkman shares her experience navigating the male dominated field of engineering while excelling as the youngest female Vice President of HDR, a multinational engineering corporation. Make sure and watch through to the end where she shares her list of “to-do’s” for women hoping to be outstanding in a professional setting.

We are so grateful to Laycee for sharing her experience and how she helps “Welcome Women to the Room”

Find useful tools to improve your professional development? Continue watching our Welcoming Women to the Room series:

Please note by using any of the links provided for your convenience, you will be leaving Fidelis Wealth Advisors website. The hyperlinks are to websites and servers maintained by third parties. We do not control, evaluate, endorse, or guarantee content found in those sites. Your use of such sites is at your own risk.

This blog is general communication being provided for informational purposes only. This information is in no way a solicitation or offer to sell securities or investment advisory services. It is educational in nature and not to be taken as advice or a recommendation for any specific investment product or investment strategy. This does not contain sufficient information to support an investment decision. Any investment or investment strategy mentioned may not be suitable for all investors or in their best interest. Statistical information, quotes, charts, references to articles or any other quoted statement or statements regarding market or other financial information is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. All rights are reserved. No part of this blog including text, graphics, et al, may be reproduced or copied in any format, electronic, print, et al, without written consent from Fidelis Wealth Advisors, LLC. Fidelis Wealth Advisors does not provide legal or tax advice. Please be advised to consult with your investment advisor, attorney or tax professional before making any investment decisions.

2023 Outlook

Posted on

By: Jeff Bullock

As we turn the page to 2023 and away from one of the worst years in both equity and credit markets in decades, we examine what happened, the policymaker response, and what that means for 2023 and beyond.

What Happened & The Response

After nearly a decade of money printing and central bank balance sheet expansion, inflation finally reared its ugly head. The decision to shut down the economy in 2020 due to Covid-19 led to the passing of unprecedented rescue packages by lawmakers, as well as direct central bank intervention in markets which had never happened before at this level. With a zero-interest rate policy (i.e., free money), a buyer of last resort (i.e., the Fed), and forgivable loans available to many businesses (i.e., PPP loans, etc), global markets and the economy seemingly went into extreme expansion mode. This all lasted for about 18 months before the inflation boogeyman came to life.

The Fed made many missteps along the way. First, they were very late to the game – one example is that they were still fueling inflation by directly buying bonds in the market as late as March 2022, when inflation was already at 8.5%. They then pivoted from a multi-decade policy of “easy money”, to extreme hawkishness, in a matter of days.

Jay Powell, the Fed Chair, went from saying, “We’re not even thinking about thinking about raising rates,” to one of the most aggressive rate-raising endeavors in decades. A pivot like this is nothing short of a massive misstep in their policy. As reported inflation hit 9.1% in June, the restrictive nature of their policy increased. The latter part of the year consisted of 0.75% rate rises every month to try and slow the economy down. The current Fed Rate went from 0.25% to 4.75% by year-end. Truly unprecedented.

Make no mistake, the Fed is trying to cause a recession. That’s the only true way to slow down inflation. All the discussion about a “soft landing” is simply a different way of saying they are trying to slow the economy down without causing a recession, or perhaps only causing a mild recession. If they overshoot and cause a “hard landing”, then we can expect more than a mild recession.

Why did the stock market have so much volatility in 2022? Very simply, it’s trying to figure out if the economy will have a hard or soft landing. The big daily, weekly, and monthly moves were all driven by news that either made investors react in extreme ways.

2023 Outlook

Despite the bad year in the stock market, most companies actually grew in 2022. Yes, you heard me correctly. Bottom-line earnings for the stock market increased in 2022 compared to 2021. Then why did the market fall nearly 20%?

Valuations/Multiples. The price of any company, or the stock market as a whole, is a function of two inputs: (1) Earnings and (2) the Multiple that investors are willing to pay for those earnings.

In 2022, despite companies delivering strong earnings, valuations dropped due to all of the uncertainties surrounding the economy. In other words, investors were not willing to pay as high of a multiple for their equity exposure in 2022 that they were willing to do in years past.

If 2022 was the year of the multiple revaluation, then 2023 will be the year of earnings.

It’s important to remember that nearly three-quarters of GDP is Consumer Consumption; i.e., you and me spending money. This drives company growth. If consumers (you and me) keep spending at the rate we have, despite the added price inflation, then company earnings will continue to stay strong. However, if consumers decide to cut back, delay a vacation, or substitute higher quality goods with lower ones, then we probably see a slowdown in the economy.

The market is currently in a “wait and see” mode. It’s not pricing in a deep or even mild recession, but at the same time, it’s not pricing in a strong economic outlook. Will inflation continue to come down? Will 4th Quarter earnings beat expectations? Will the Fed be able to hit the breaks on raising interest rates?

These are all the questions that will drive the earnings narrative for 2023.

Portfolio Positioning

With all of that said, how do we position portfolios in an environment like this for those who have exposure?

On the equity side, we continue to tilt toward the value style of equities with an emphasis on strong dividend-paying companies. We have been positioned this way since early 2022, which has been good, and continue to like this area to start the year.

On the fixed income side, we continue to focus on short-to-mid duration and high quality credit. We have been positioned on the short-end of the duration spectrum for over a year now, which has been a good place to be. We continue to favor short-duration over long.

On the alternative side, we continue to like 1st lien private credit where it makes sense in a portfolio.

Summary

We expect the first part of 2023 to continue to be choppy in equity markets with elevated volatility still playing a role in portfolios. As inflation, unemployment, and earnings data role in, markets will adjust and re-price expectations.

Bull Case: The bull case is a “soft landing” from the Fed and lower inflation. This will allow interest rates to stabilize, modest growth, and even the small potential for multiple expansion.

Bear Case: The bear case is a “hard landing” from the Fed and sticky inflation. This will cause interest rates to stay elevated which will mute growth and potentially cause multiples to fall even more.

Base Case: Somewhere in-between the “soft” and “hard” landing. Unemployment will then take center stage as the economy will look toward a recovery in 2024.

Without using too many superlatives, 2022 was truly an unprecedented year in markets. We are confident in our approach and watch market each day looking for opportunities.

As always, feel free to give us a call to discuss.

This blog is general communication being provided for informational purposes only. This information is in no way a solicitation or offer to sell securities or investment advisory services. It is educational in nature and not to be taken as advice or a recommendation for any specific investment product or investment strategy. This does not contain sufficient information to support an investment decision. Any investment or investment strategy mentioned may not be suitable for all investors or in their best interest. Statistical information, quotes, charts, references to articles or any other quoted statement or statements regarding market or other financial information is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. All rights are reserved. No part of this blog including text, graphics, et al, may be reproduced or copied in any format, electronic, print, et al, without written consent from Fidelis Wealth Advisors, LLC. Fidelis Wealth Advisors does not provide legal or tax advice. Please be advised to consult with your investment advisor, attorney or tax professional before making any investment decisions.

Should I DIY my Investments?

Posted on

By: Jeff Bullock

Should I DIY my Investments?

I get asked all the time if a DIY approach to investing is the right method. There’s no clear-cut answer. For some with an investment background or education, it might make sense. For others, hiring an advisor is really the only way to create peace of mind. For those who go about the DIY approach, generally it’s a game of trade-offs. The most common trade-offs revolve around the time commitment, cost, access to trusted help, financial understanding, and deal flow.

While there are many ways to approach your money management, here are three things to think about before you DIY your own investments:

Co-Pilot:

The best-trained pilots need a co-pilot. The best quarterbacks in the NFL need a QB Coach. Even if you feel comfortable with the investment landscape, does it makes sense to have a co-pilot, especially if that co-pilot is up-to-date on industry news, landscape and innovation?

I meet with many people each year who are fully capable of taking a DIY approach to their finances, but generally due to their busy schedules, they aren’t able to dedicate the proper amount of time needed to make the best decisions. In many instances, the purpose of a co-pilot is to ensure the best decision is made, not just a good one.

Innovation:

Contrary to some thinking, there is a ton of innovation happening in the investment world. New products and better ways to get access to certain asset classes are being created and rolled out each year. A great advisory team will be meeting with industry partners regularly to stay ahead of the innovation curve.

Access:

Deal flow and access to opportunities can be a big trade-off when taking a DIY approach. Most financial institutions operate through “channels” to distribute their products and investment opportunities. In many instances, certain investment opportunities are only available through an advisor because that is the only channel by which the opportunity is being distributed.

Is it cheaper to DIY your investments? On the surface, it may feel that way depending on your approach, as long as you are willing to accept the tradeoffs.

For example, 2022 has obviously been a volatile year in markets. However, there are many investments that have positive returns this year, but are only available through the advisor channel, and can’t be accessed by the DIY investor. These investments have been an anchor to our portfolios during these volatile movements. My job is to help people make better decisions and continuously improve. If being the pilot or co-pilot through your financial journey can help you make better decisions, then perhaps there’s a place for an advisor in your life.

This blog is general communication being provided for informational purposes only. This information is in no way a solicitation or offer to sell securities or investment advisory services. It is educational in nature and not to be taken as advice or a recommendation for any specific investment product or investment strategy. This does not contain sufficient information to support an investment decision. Any investment or investment strategy mentioned may not be suitable for all investors or in their best interest. Statistical information, quotes, charts, references to articles or any other quoted statement or statements regarding market or other financial information is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. All rights are reserved. No part of this blog including text, graphics, et al, may be reproduced or copied in any format, electronic, print, et al, without written consent from Fidelis Wealth Advisors, LLC. Fidelis Wealth Advisors does not provide legal or tax advice. Please be advised to consult with your investment advisor, attorney or tax professional before making any investment decisions.

Three Things to Ask Your Advisor in November

Posted on

By: Jeff Bullock

Three Things to Ask Your Advisor in November

Being a wealth advisor is a lot like navigating a ship through the ocean. While you can prepare for all the different types of elements you may encounter, ultimately, you have to navigate in whatever weather appears that day. Without a doubt, 2022 has been an unprecedented year for ‘financial weather’ disrupting many portfolios and personal goals. Despite what has happened, a great wealth advisor is always adjusting and will see the landscape as it appears today, and make decisions based on the present situation. As we near the end of the year, there are potentially a few things that can be done to re-position your portfolio for next year.

Everything starts with good communication with your wealth advisor. I would suggest you call your advisor this month, and along with other questions you might have, ask them these three questions:

Have you done any tax-loss harvesting in my portfolio this year?

The current tax code allows you to “carry forward” capital losses indefinitely into the future, as well as deduct up to $3,000 of those losses in the current year. After a year like this where many financial securities are down, harvesting losses can be an effective strategy to get a small deduction today, while also banking those losses for use against gains in future years.

Are you helping me mitigate capital gains distributions?

At the end of every year, many mutual funds and some ETFs will distribute something called a “capital gains distribution.” This is where the fund will pass through a portion of the proceeds from sales that occurred within the fund, to the fund holder. If you own a mutual fund or ETF that does this type of distribution, then it will be a taxable event, which in a year like this feels even worse. There are strategies to mitigate these types of distributions that your advisor should already should be implementing.

Does a Roth IRA conversion make sense this year?

Perhaps you have money in a Traditional IRA that you’ve always wanted to convert to a Roth IRA, but have never wanted to pay the tax. With the market being down so much this year, it might make sense to ask your advisor if this is a good year to convert these funds to a Roth IRA. There will be a tax associated with this conversion, but this may be an opportunity to explore if it makes sense for your tax situation.

Before you get too busy with holiday gatherings and other year-end events, call your advisor and check-in on your portfolio. Despite the difficult year in markets, there are still ways that you can set your investments up for a better tomorrow.

This blog is general communication being provided for informational purposes only. This information is in no way a solicitation or offer to sell securities or investment advisory services. It is educational in nature and not to be taken as advice or a recommendation for any specific investment product or investment strategy. This does not contain sufficient information to support an investment decision. Any investment or investment strategy mentioned may not be suitable for all investors or in their best interest. Statistical information, quotes, charts, references to articles or any other quoted statement or statements regarding market or other financial information is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. All rights are reserved. No part of this blog including text, graphics, et al, may be reproduced or copied in any format, electronic, print, et al, without written consent from Fidelis Wealth Advisors, LLC. Fidelis Wealth Advisors does not provide legal or tax advice. Please be advised to consult with your investment advisor, attorney or tax professional before making any investment decisions.

Cash & Treasuries

Posted on

By: Jeff Bullock

Cash & Treasuries

While rising interest rates makes it more expensive to borrow money for future purchases, it has created some interesting opportunities to invest and make interest. Banks are slowly starting to raise the interest they pay on checking, savings, and CDs, but they still significantly lag the U.S. Treasury market.

U.S. treasuries are bonds, issued and guaranteed by the U.S. Government, to fund our national expenses. The treasury market has an estimated size of $25 trillion. These treasuries can be purchased for one week or 30 years depending on your personal time horizon. With the Federal Reserve raising interest rates, the yield on U.S. treasuries has also risen. Many of these treasuries function similar to that of a bank CD, in that, you buy it for a certain period of time, and at the maturity date, you receive your original amount plus interest back. It’s very simple.

Below are the yields, as of today, of treasury bills and notes:

1 month: 2.70%

3 month: 3.20%

6 month: 3.80%

1 Year: 4.00%

The yields change daily, but for a number of months now, if you were to compare these yields to what most banks are offering in savings accounts or CDs, these are significantly higher. If you are worried about the stock market or are looking to get a better return than your bank savings account, the U.S. Treasury market might be worth a look. Markets have been quite volatile digesting news from many angles.

As always, please call with any questions or if you simply want to get our views.

This blog is general communication being provided for informational purposes only. This information is in no way a solicitation or offer to sell securities or investment advisory services. It is educational in nature and not to be taken as advice or a recommendation for any specific investment product or investment strategy. This does not contain sufficient information to support an investment decision. Any investment or investment strategy mentioned may not be suitable for all investors or in their best interest. Statistical information, quotes, charts, references to articles or any other quoted statement or statements regarding market or other financial information is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. All rights are reserved. No part of this blog including text, graphics, et al, may be reproduced or copied in any format, electronic, print, et al, without written consent from Fidelis Wealth Advisors, LLC. Fidelis Wealth Advisors does not provide legal or tax advice. Please be advised to consult with your investment advisor, attorney or tax professional before making any investment decisions.

Brandon Waite

PROFESSIONAL

Brandon is new to the wealth management business, however, he brings many skills useful to the profession because of his prior experience. Brandon has worked in the accounting world auditing hedge funds, venture capital firms, and low-income housing organizations. Assessing business risk and financial GAAP accounting has been his primary focus. He is passionate about the world of finance and helping individuals accomplish their financial dreams.

Brandon graduated from Brigham Young University- Idaho with a bachelor’s degree in accounting. Additionally, he holds two professional designations, Certified Public Accountant (CPA) and Certified Fraud Examiner (CFE).

PERSONAL

He lives in Castle Rock with his wife Emily, and their three daughters. Most of his free time consists of taking his daughters to the park, enjoying all types of sports, and watching movies.

Bailey Marudas-Jones

Bailey Marudas-Jones joined Fidelis Wealth Advisors in 2024, where she supports the back office by managing client onboarding and ensuring compliance. She also helps alleviate the team’s workload by handling various administrative tasks and processes. With a deep commitment to efficiency and excellence, Bailey is excited to contribute to the team’s success and help clients navigate their financial journeys at Fidelis Wealth Advisors. Bailey grew up in Littleton, Colorado, where she still lives. In her free time, she enjoys watching old movies, reading, and learning to sew. She also loves spending time with her family and friends

Karley Winder

PROFESSIONAL Before joining the firm in 2022, Karley ran several local businesses, selling products in the Castle Rock area and online. Her passion for business inspired her to earn a degree in Financial Management from the University of Colorado Denver. At Fidelis, she has specialized in 401(k) plans and has also developed expertise in client-facing roles as a paraplanner. She holds a Series 65 license and plans to earn her Certified Financial Planner® designation. She is committed to providing a valuable experience that brings clients peace of mind.

PERSONAL

Karley is a Colorado native and grew up here in Castle Rock. She enjoys riding her horse, Dante, hiking and mountain biking the beautiful state of Colorado, and playing electric guitar.

Rilee Erickson

PROFESSIONAL

Rilee began working in the financial services industry in 2017 as an associate specializing in property and casualty insurance, as well as life insurance. Since joining Fidelis Wealth Advisors she has taken on a paraplanner roll, providing life insurance support, as well as client and operations support. She also hopes to obtain her own Certified Financial Planner® designation in the years to come. Rilee’s passion in the industry is helping people protect their family and their future.

PERSONAL

Rilee graduated from the University of Wyoming with a Bachelor of Science in Agribusiness and Horticulture Science. She is a Wyoming native, growing up on the family cattle ranch in Lander, Wyoming, and now resides in Green River, Wyoming with her husband and two boys. Rilee enjoys spending a lot of time outdoors and exploring the beautiful and rugged Wind River Range.

Tina Jessick

PROFESSIONAL Tina first began her accounting career in 2019 as an Intern at an accounting firm in Wichita, KS. She started working at Fidelis Wealth Advisors as an Administrative Assistant spring of 2025. Tina hopes to assist in helping clients achieve their financial goals long-term and looks forward to making a difference at Fidelis Wealth Advisors.

PERSONAL Tina is currently attending Wichita State University in pursuit of two degrees in Finance and Accounting. She is a Kansas native, growing up in city known as the “Air Capital of the World”. She now resides in Castle Rock, Colorado with her husband and three kids. When she’s not running after her kids, she enjoys hiking, crafting, pottery, dance and baking.

Fidelis Wealth Advisors has a strategic partnership with RIA Innovations, a Division of NWAM, LLC. RIA Innovations provides administrative support services for registered investment advisors nationwide. This service is under the direction of Nelly Mubashi, the Chief Operating Officer.

NWAM, LLC, dba Northwest Asset Management & RIA Innovations is an SEC registered investment adviser. NWAM, LLC dba Northwest Asset Management & RIA Innovations and Fidelis Wealth Advisors, LLC are not affiliated companies.

Gabriel Jones

PROFESSIONAL Gabe started with Fidelis Wealth Advisors as an Investment Research Assistant in 2018, and has an intense passion for investment research.

PERSONAL Gabe is currently in college to obtain his Bachelors in Finance, and enjoys spending time outside of work hiking and reading.

Dawn Folmer

PROFESSIONAL Dawn Folmer comes to Fidelis Wealth Advisors with a background in the finance industry, having previous experience with a registered investment advisory firm in Denver. Dawn is a recent graduate of Colorado State University Global, earning a Bachelor of Science degree in Organizational Leadership. As a skilled financial planning assistant, she enjoys the rewarding feeling of helping people reach their financial dreams and retirement goals.

PERSONAL Dawn is a Colorado native and resides in Castle Rock with her family, where they enjoy being adventurous and active in the outdoors. Additionally, she is passionate about travel, food, and playing golf.

Jeff Bullock

PROFESSIONAL Jeff joined Fidelis Wealth Advisors after spending nearly 10 years working at J.P. Morgan Wealth Management in their Private Bank. As Chief Investment Officer, he is responsible for the overall investment strategy, portfolio construction, and market insights for clients.

Jeff held various roles during his decade at J.P. Morgan, including working as an investment specialist on their trading desk, where he was responsible for managing and trading investment portfolios for High Net-Worth families and non-profit foundations throughout the Rocky Mountain region. Jeff helped co-manage over $4.0 billion of investment assets and gained broad experience in portfolio construction and investment strategy, as well as in-depth knowledge in a variety of asset classes and markets. In recent years, Jeff was part of the leadership team that trained new advisors and established an expansion office in Utah.

Jeff loves helping people with their money-related questions and management. Very simply, his goal is to help others continuously improve their financial situation, regardless of the current condition. His framework centers around sound advice and proper decision-making by engaging in honest discussion and taking a long-term approach.

PERSONAL Jeff holds a B.S. in Accounting from Brigham Young University. He is a native to Colorado and loves playing golf and being outdoors. He lives in Highlands Ranch with his wife Nicole, and their two children.

PROFESSIONAL Lorie began working in financial services in 2013 with a Registered Investment Advisory firm in South Denver. She started as a paraplanner and provided technology and operations support before transitioning to a Client Services Manager role with Empower Retirement. There she managed a book of 300+ Core Market plans before joining Fidelis Wealth Advisors.

Lorie enjoys the challenges presented by financial planning and is rewarded by helping clients thoroughly understand the complexities of finance so they can be better informed and in control of their planning.

In addition to securities licenses, she holds health, life, accident, property, and casualty insurance licenses in the state of Colorado and completed her CERTIFIED FINANCIAL PLANNER™ designation from the CFP® Board of Standards. She is also a member of the Financial Planning Association (FPA).

Lorie recently launched the “Fearless Females” podcast, providing a unique space for empowering discussions that inspire women in the financial services industry and beyond. Through insightful interviews and stories, she fosters a community where challenges are met with resilience, amplifying female voices and demonstrating her dedication to fostering inclusivity and fearlessness in finance.

PERSONAL Lorie graduated from Colorado State University with an MBA. She enjoys running and has participated in several marathons and half-marathons around the country. She also enjoys hiking with her family, traveling with her husband David and their five children, and working with the cub scout and boy scout programs, including volunteering with the district.